Skip to content

Skip to content

Choosing a Medicare plan is one of the biggest financial decisions of your retirement, and most people make it without a clear checklist. The questions to ask before choosing a Medicare plan aren’t complicated, but the answers are specific to you, your doctors, your medications, and where you live. Getting the answers wrong costs real money, and some mistakes are hard to undo.

Here are the questions that actually matter before you sign anything.

Are Your Current Doctors Covered by This Plan?

Your doctors being in-network is the single most important question to answer before choosing any Medicare plan. If you choose a Medicare Advantage plan and your primary care doctor or specialists aren’t in the network, you either pay out-of-network rates or find new providers. Neither is a small inconvenience after years of established care.

Original Medicare lets you see any doctor in the country who accepts Medicare patients, which is the vast majority of physicians. Medicare Advantage plans restrict you to a defined network, and that network can change from year to year. A doctor who was in-network when you enrolled may not be in-network next year.

Before enrolling, call each of your doctors’ offices directly and ask whether they participate in the specific plan you’re considering. Don’t rely on the insurer’s online directory alone. Directories are sometimes out of date, and a phone call takes five minutes and can save you thousands.

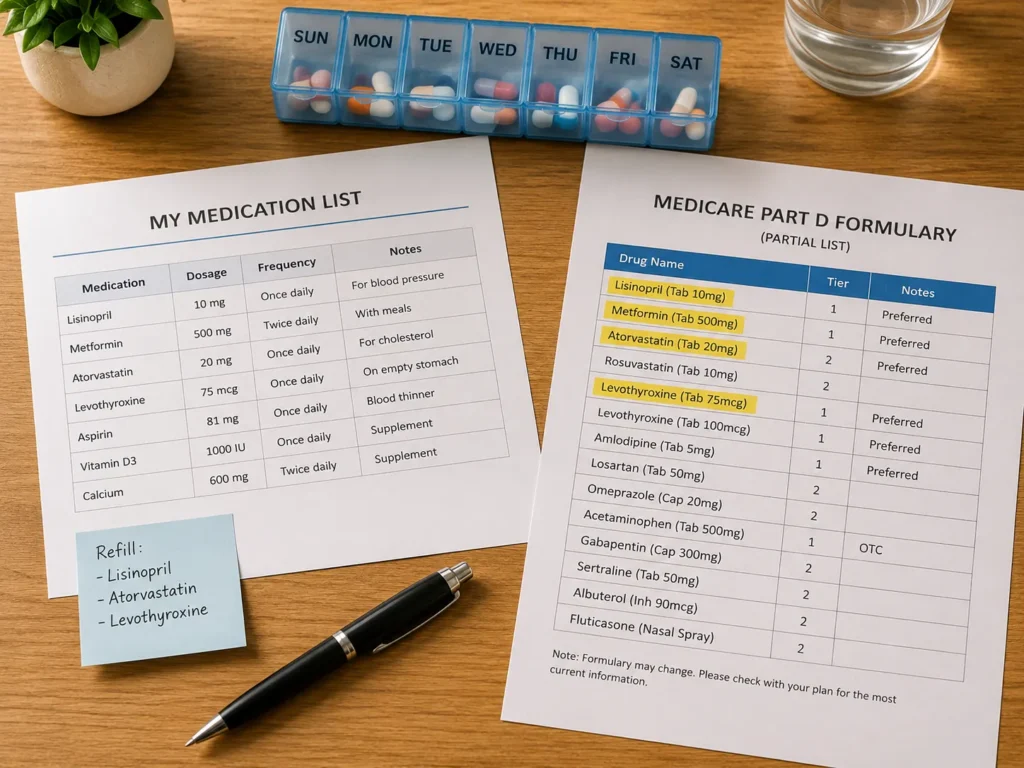

Are Your Prescriptions Covered on This Plan’s Formulary?

Each Medicare plan that includes drug coverage, whether a standalone Part D plan or a Medicare Advantage plan with drug coverage built in, maintains a formulary, which is a list of covered medications and the tier at which each is covered. Your prescriptions need to be on that list before you commit to a plan.

Formularies are not standardized across plans. A medication your doctor has prescribed for years may be on Tier 1 of one plan (low copay) and Tier 4 of another (high copay), or not covered at all. Before enrolling, run every medication you take through the plan’s formulary lookup tool on medicare.gov or ask a broker to do it for you.

Also check whether the plan requires step therapy for any of your medications. Step therapy means the insurer requires you to try a cheaper drug first before they’ll cover the one your doctor prescribed. If you’re already on a stable, effective medication, that requirement can be a significant disruption.

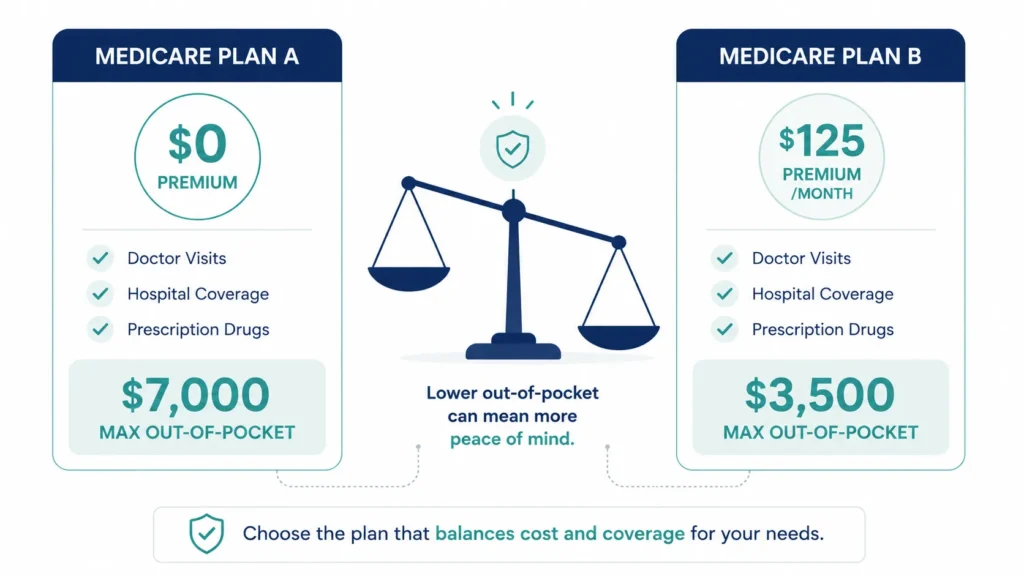

What Will This Plan Actually Cost You in a Bad Year?

The monthly premium is the cost people focus on, but for Medicare plans the premium is often the least important number. The questions that reveal the real cost of a plan are about what you’ll pay when you actually use it.

For Medicare Advantage plans, ask about the annual out-of-pocket maximum for in-network care. In 2025, the maximum cap is $9,350 for in-network services, according to KFF. But many plans set their maximum lower than that, and the difference matters enormously if you have a serious health event. A plan with a $3,500 out-of-pocket maximum and a slightly higher premium may be far cheaper in a bad year than a $0 premium plan with a $7,000 cap.

For Original Medicare, there is no out-of-pocket maximum built in. That’s why Jonathan Potter, who has guided Medicare clients since 2006, consistently recommends pairing Original Medicare with a Medigap supplement plan. The combination typically costs more per month, but it eliminates the open-ended financial exposure that Original Medicare alone carries.

Review your Medicare plan options with a broker who can show you the full-year cost estimate under different health scenarios, not just the premium.

Does This Plan Cover You If You Travel or Spend Time in Multiple States?

If you split your time between states, travel frequently, or spend winters somewhere other than your primary home, coverage portability matters a great deal. Original Medicare covers you at any Medicare-accepting provider nationwide, which makes it well-suited for people who move around.

Most Medicare Advantage plans limit your coverage to a defined service area. If you leave that area, your coverage generally applies only to emergencies. Routine care, specialist visits, and non-emergency hospitalizations outside the plan’s region may not be covered or may be subject to significantly higher cost-sharing.

Before enrolling in a Medicare Advantage plan, ask specifically about coverage outside the plan’s service area, including whether the plan covers emergency care nationally and internationally. Some plans, particularly PPO-style plans, offer broader out-of-network benefits than HMO plans. The answer to this question may determine which plan type fits your lifestyle.

What Happens to Your Coverage During the Annual Enrollment Period?

Medicare plans can change their benefits, premiums, formularies, and networks every year, and those changes take effect January 1. The Annual Enrollment Period runs from October 15 to December 7, giving you a window to review your plan and switch if something has changed that affects your care.

Many people enroll in a plan once and never revisit it. That’s a mistake. A medication that was covered last year may be dropped from the formulary. Your doctor may leave the network.

The out-of-pocket maximum may increase. These changes are communicated through an Annual Notice of Change letter your plan sends in September, and it’s worth reading every word.

If you’re not sure whether your plan still makes sense, that’s exactly the right time to sit down with a broker and run a comparison before the December 7 deadline.

FREQUENTLY ASKED QUESTIONS

Can I switch Medicare plans after I enroll?

Yes, but outside of specific enrollment windows, your options are limited. The Annual Enrollment Period from October 15 to December 7 allows you to switch between Medicare Advantage plans or between Medicare Advantage and Original Medicare. If you want to add a Medigap supplement plan outside your initial enrollment period at 65, insurers may use medical underwriting, which means they can charge more or deny coverage based on your health history.

How do I find out what my Medicare plan covers?

Every Medicare plan is required to provide a Summary of Benefits and an Evidence of Coverage document that details exactly what is covered, at what cost, and under what conditions. These are available on the plan’s website or on medicare.gov. For drug coverage, each plan’s formulary is also searchable on medicare.gov by plan name and medication.

Is it worth talking to a broker before choosing a Medicare plan?

Yes, and it costs you nothing. An independent broker can compare multiple plans in your area side by side, run your specific medications through each plan’s formulary, and flag cost differences you might miss reviewing plans on your own. The broker is paid by the carrier, not by you, which means the comparison comes at no charge.

The questions to ask before choosing a Medicare plan aren’t difficult, but the answers are personal and the stakes are high. A plan that looks identical to another on the surface can cost thousands more in a year when your health actually needs it. Connect with Beacon Insurance Advisors Connect with Beacon Insurance Advisorshttps://beaconinsuranceadv.com/#contact to get a side-by-side comparison tailored to your doctors, your medications, and your retirement budget.